Klaus Vedfelt/DigitalVision via Getty Images

|

Q1 2025 |

YTD |

1-Year |

3-Year |

5-Year |

Inception† |

|

|

Leaven Partners, LP |

14.2% |

14.2% |

9.8% |

35.0% |

101.2% |

65.4% |

|

S&P 500 (SPXTR) |

-4.2% |

-4.2% |

8.2% |

27.7% |

130.8% |

128.3% |

|

MSCI EAFE (EFA) |

8.0% |

8.0% |

5.5% |

19.2% |

75.1% |

42.9% |

|

Vanguard Total World (VT) |

-0.9% |

-0.9% |

6.9% |

20.2% |

102.4% |

77.8% |

|

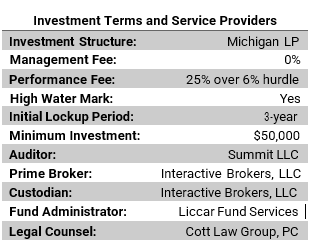

Leaven Partners, LP are time-weighted gross cumulative returns (unaudited) provided by our prime broker, Interactive Brokers. Performance data, (net of all fees and expenses), for each partner, is provided by Liccar Fund Services. †Trading began on March 16, 2018. |

Dear Partners,

In the first quarter of 2025, total fund assets appreciated by 14.2%. For the three-year period, the fund is up 35.0%1 compared to the S&P 500 return of 27.7%.

I want to thank everyone for spending a Saturday morning together last month for our annual meeting. It was truly a delight for me to host, and it is an honor to be a part of such wonderful people!

As discussed in the meeting, 2025 has started off well, with the fund finishing the quarter up over 14% gross. We reviewed some of the key contributors to fund returns, including a significant gain in Nakayo, Inc. (6715:TSE).

Founded in 1944, Nakayo is a Japanese company with around 750 employees. They manufacture communication equipment used in traditional voice communication in addition to IP telephone technology. Like so many small-cap companies in Japan, this is a sleepy company with a long history of profitability. Being keen on fundamental momentum, I bought shares of the company after it began showing noticeable improvements in its profitability and capital efficiency. At the time of purchase, the company had around $22 million in cash, $130 million in assets with no debt, and was trading on the stock market for $35 million.2 My conversative estimate of the liquidation value was $58 million. I made it a material position in the fund. As luck would have it, not long after owning the stock, Ai Holdings (3027:TSE), which owned about 8% of the stock at the time, made a tender offer for the remaining shares of the company at ¥2,550 per share. We sold our entire holding at around ¥2,535 per share, for a gain of about 130%. There are many more undervalued companies like Nakayo in Japan, presenting ripe opportunities.

What a difference a few weeks can make! Since our annual meeting a brief time ago, markets have ramped up the volatility to dizzying heights. The commonly used gauge for market volatility is the Cboe Volatility Index (VIX). You might think of it as Wall Street’s “fear gauge.” The VIX has reached crisis level, peaking at 60 – a level usually only seen during major market sell-offs like the COVID-19 period and the 2008 financial crisis.

Markets hate perceived uncertainty. President Trump’s geopolitical war on an economic front has pushed the boundaries on POTUS’s ability to wield tariffs3 as Thor’s hammer. It remains undetermined if the President’s actions are simply a negotiating tactic or whether these onerous tariffs will hold. Whatever the case may be, it has introduced too much perceived uncertainty. And uncertainty begets volatility. On April 9th, the market surged 9.5% — the largest single-day gain since 2008 — following President Trump’s announcement of a 90-day tariff pause, only to fall sharply by 3.5% the next day. We may experience more volatility in the days to come.

Although volatility in the stock market is worrisome, volatility in the bond market may be more troubling. In short, both the bond market and the stock market are in decline, suggesting that there may be a liquidity crisis in the financial sector. For example, there currently are some rumblings about concern of the instability of “the basis trade.” If you have not heard of the basis trade, do not worry, you are not alone! The basis trade is a standard tool used by asset managers to get short-term Treasury-like returns without having to put up all the money to own the T-Bill outright. Instead of borrowing money the traditional way, asset managers can use financial markets to “borrow” money by buying Treasury futures instead. Hedge funds have risen in recent times4 to take up the opposite side of that trade by borrowing significant sums of money, selling the futures (that the asset managers are buying) and owning the underlying T-Bill. This action of being short futures and long the underlying provides the hedge funds with a small spread for their services. In return, asset managers pay a bit of premium but get Treasury-like returns. The size of the basis trade is enormous, with estimates suggesting it accounts for around $800 billion to $1 trillion in notional value, making it a significant component of the financial system. When the water is calm, everyone is happy, and each participant is getting adequately compensated. The problem of course is when volatility spikes and the short position is not adequately ‘hedged’ by the underlying holdings—which creates margin calls, forcing hedge funds to sell T-Bills to pay down their short positions. If volatility goes haywire, that is a problem—just ask Long-Term Capital Management.

Think of our financial system as a finely tuned Ferrari. Everything is structured with fine precision down to the last rivet; when the weather is good, performance is flawless. But start tinkering with a component in the car and you may have secondary and tertiary effects that could cause malfunctions in other areas of the car that are problematic, even deadly. POTUS is tinkering.

In all, increased levels of uncertainty coupled with an overvalued stock market and calls for an “imminent”5 recession make for interesting times to say the least; a ready supply of Dramamine may be in order.

Needless to say, I have no idea what will happen next. Regardless of the outcome, executing our strategy with patience with an eye towards mitigating risk is the path forward.

As always, my own capital is heavily invested alongside yours, aligning my incentives with yours.

In Closing

I am grateful for your participation in Leaven Partners, and that you have entrusted me with managing your assets. I look forward to reporting to you at our next quarter-end.

In the meantime, if there is anything I can do for you, please do not hesitate to contact me.

Sincerely,

Brent Jackson, CFA

|

Footnotes 1 This equates to an approximate 10.5% annualized gross return for the 3-year period. 2 Please note these estimates are based on conversion from Japanese yen to US dollar. 3 Technically, the House of Representatives has Constitutional authority on issuing tariffs, not POTUS. 4 It used to be primarily investment banks. 5 https://www.hussmanfunds.com/comment/mc250404/ DISCLAIMER The information contained herein regarding Leaven Partners, LP (the “Fund”) is confidential and proprietary and is intended only for use by the recipient. The information and opinions expressed herein are as of the date appearing in this material only, are not complete, are subject to change without prior notice, and do not contain material information regarding the Fund, including specific information relating to an investment in the Fund and related important risk disclosures. This document is not intended to be, nor should it be construed or used as an offer to sell, or a solicitation of any offer to buy any interests in the Fund. If any offer is made, it shall be pursuant to a definitive Private Offering Memorandum prepared by or on behalf of the Fund which contains detailed information concerning the investment terms and the risks, fees and expenses associated with an investment in the Fund. An investment in the Fund is speculative and may involve substantial investment and other risks. Such risks may include, without limitation, risk of adverse or unanticipated market developments, risk of counterparty or issuer default, and risk of illiquidity. The performance results of the Fund can be volatile. No representation is made that the General Partner’s or the Fund’s risk management process or investment objectives will or are likely to be achieved or successful or that the Fund or any investment will make any profit or will not sustain losses. As with any hedge fund, the past performance of the Fund is no indication of future results. Actual returns for each investor in the Fund may differ due to the timing of investments. Performance information contained herein has not yet been independently audited or verified. While the data contained herein has been prepared from information that Jackson Capital Management GP, LLC, the general partner of the Fund (the “General Partner”), believes to be reliable, the General Partner does not warrant the accuracy or completeness of such information. |

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.